How Yellow Card is Redefining Cross-Border Payments in Africa

Cryptocurrency isn’t just about speculation; it’s reshaping how we move money. In Africa, where the need for affordable, fast, and reliable cross-border payments is acute, Yellow Card has emerged as a game-changer. By leveraging stablecoins and embracing a customer-first approach, Yellow Card is simplifying remittances and empowering millions across the continent.

Introduction

Africa’s remittance market is an economic powerhouse, with an estimated $95 billion flowing into the continent each year. These funds play a vital role in supporting families, paying for education, and driving small businesses. Yet, despite its importance, the remittance system is far from perfect. Traditional channels—banks and money transfer operators—are bogged down by sky-high fees and painfully slow processes. Imagine sending $200 to your loved ones in Ghana, only to lose nearly 8% of it to fees. According to the World Bank, that’s the harsh reality for many Africans, making this the most expensive remittance corridor in the world.

This is where Yellow Card steps in, flipping the script on outdated financial systems. Born out of frustration with these inefficiencies, Yellow Card is a platform dedicated to slashing costs and breaking down barriers to financial access. By leveraging cryptocurrency—specifically stablecoins—the company is rewriting the rules of remittances.

Founded in 2016, Yellow Card has rapidly grown to become the largest and first licensed stablecoin on/off ramp in Africa. Its mission? To make remittances not just faster and more affordable, but also accessible to everyone, whether you’re in a bustling city like Nairobi or a rural village in Malawi. With a few taps on your phone, you can send money across borders without the stress of exorbitant fees or long wait times. It’s not just about transactions; it’s about empowering individuals and families to thrive.

Yellow Card’s journey is a testament to the power of innovation. From a simple idea sparked by witnessing the struggles of a man trying to send money home, it has grown into a trailblazer in Africa’s crypto space. And as the continent’s appetite for digital solutions grows, Yellow Card is leading the charge, proving that financial inclusion isn’t just a dream—it’s a reality within reach.

The Vision Behind Yellow Card

Yellow Card’s mission is simple yet powerful: financial inclusion for all. They believe in empowering individuals to take control of their money while promoting global financial freedom across Africa. The vision isn’t just about technology; it’s about creating opportunities.

By focusing on equality of access, Yellow Card ensures that a farmer in Uganda and a student in South Africa have the same tools to participate in the digital economy as anyone else in the world. It’s this mission that drives their innovative solutions.

The Yellow Card Journey

Yellow Card’s story isn’t just about numbers or technology; it’s about people. The spark that ignited the company’s mission came in 2018 when Chris Maurice, the company’s CEO, met a man who had sent $200 from the U.S. to his family in Nigeria. The bank charged an outrageous $90 in fees—almost half of the amount sent. That moment hit Chris like a lightning bolt. How could such an essential service be so broken?

Motivated by the desire to fix this injustice, Chris teamed up with Justin Poiroux, Yellow Card’s co-founder and CTO. Together, they envisioned a platform that could provide basic financial services to everyone, regardless of where they lived or how much they earned. In 2019, Yellow Card officially launched in Nigeria with a mission to make financial inclusion a reality.

What started as a small operation quickly gained momentum. By focusing on the unique challenges faced by Africans—like limited access to banking and high transaction costs—Yellow Card grew into a trusted name. The platform didn’t just stop at Nigeria; it expanded rapidly across 20 African countries, from Kenya to South Africa, Ghana to Botswana. Today, the company serves millions of users, helping them access stablecoins like USDT, USDC, and PYUSD seamlessly.

But growth doesn’t happen in isolation. Yellow Card’s rise has been fueled by its people—over 200 dedicated team members working tirelessly to build a robust, user-friendly platform. And let’s not forget the backing of some big names in the fintech world. With over $50 million in funding from heavyweights like Coinbase, CashApp, and Polychain Capital, Yellow Card has the resources to keep pushing boundaries.

The journey isn’t just about expansion; it’s about impact. Each transaction processed by Yellow Card represents a life made easier, a barrier broken down, or an opportunity unlocked. Whether it’s a student in Tanzania paying tuition or a small business owner in Uganda importing goods, Yellow Card is making financial freedom more than just a buzzword. It’s making it real.

Products and Services Driving Change

Yellow Card is not just another crypto platform; it’s a lifeline for individuals and businesses navigating Africa’s financial landscape. The company’s products and services cater to diverse needs, whether you’re sending money to family, shielding your savings from inflation, or running a business that thrives on cross-border transactions. Here’s how Yellow Card is driving change:

1. Stablecoin Access: A Safe Haven in Volatile Times

In a continent where many currencies are plagued by instability and inflation, stablecoins like USDT, USDC, and PYUSD offer a much-needed solution. Yellow Card provides seamless access to these digital assets, allowing users to buy and sell them using local currencies.

Why does this matter? Imagine living in Zimbabwe, where hyperinflation has made saving in local currency almost pointless. Stablecoins act as a financial safe haven, preserving value and offering a reliable medium for transactions. Whether you’re a student saving for tuition or a merchant needing predictable pricing, stablecoins bridge the gap between uncertainty and financial security.

2. Yellow Pay: Remittances Made Easy

Traditional remittance systems are, let’s face it, a hassle. Between the sky-high fees and lengthy processing times, sending money from Kenya to Ghana or Nigeria can feel like running a bureaucratic marathon. Yellow Pay flips the script by leveraging stablecoins for seamless cross-border payments across 20 African countries.

Here’s how it works: You deposit local currency, convert it into stablecoins, and the recipient cashes out in their local currency. This “cash-coin-cash” model ensures that you get the best exchange rates with significantly lower fees. Plus, the process is quick—no more waiting days for funds to arrive. Whether it’s helping a friend in need or supporting family back home, Yellow Pay makes the process stress-free and affordable.

3. Trading App: Built for Everyone, Everywhere

Accessibility is at the heart of Yellow Card’s trading app. The app integrates local payment methods—mobile money, bank transfers, and even cash agents—to ensure everyone can use it, regardless of where they are.

Picture this: You’re in rural Uganda, far from traditional banking infrastructure, but with mobile money and the Yellow Card app, you can trade Bitcoin or stablecoins without breaking a sweat. The app’s intuitive design means you don’t need to be a tech whiz to get started. From urban professionals in Lagos to small-scale traders in Tanzania, the app serves everyone.

4. Commercial Trading: Solutions for Businesses

Businesses need liquidity, speed, and efficiency, especially when dealing with cross-border trade. Yellow Card’s commercial trading solutions offer exactly that. Companies can access direct trade liquidity and digital asset tools to streamline their operations. Whether it’s a textile exporter in Ethiopia or a tech startup in South Africa, Yellow Card helps businesses manage international transactions without the usual headaches.

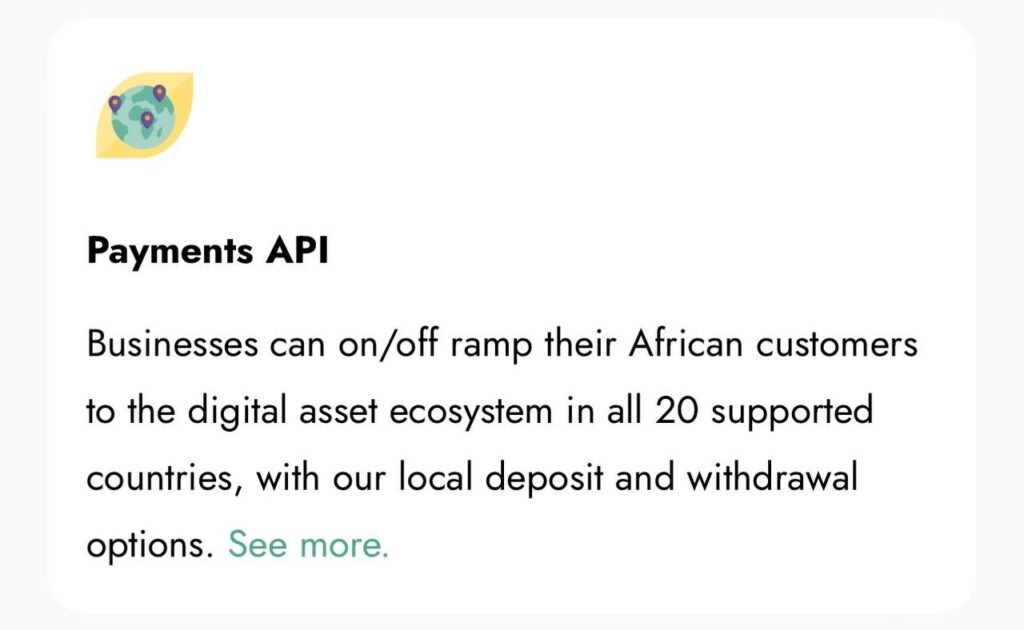

5. Payments API: Bridging the Gap for Businesses

Yellow Card isn’t just focused on individual users; it’s also empowering businesses through its Payments API. This tool allows companies to integrate crypto payments directly into their platforms, making it easier for their customers to move between fiat and digital currencies.

Take, for instance, an e-commerce site in Ghana. With Yellow Card’s Payments API, the site can accept crypto payments from customers in Kenya, instantly converting those payments into Ghanaian Cedis. This flexibility is a game-changer for businesses looking to tap into Africa’s growing digital economy.

From stablecoins to remittances, from personal trading to commercial solutions, Yellow Card is building a financial ecosystem that’s inclusive, innovative, and tailored to Africa’s unique challenges. These products and services don’t just meet the continent’s needs—they exceed them, proving that with the right tools, financial freedom is more than just a dream.

Regulatory Leadership and Compliance

Navigating Africa’s fragmented regulatory landscape is no walk in the park. Each country comes with its own unique rules, challenges, and complexities. But Yellow Card has not only taken this challenge head-on—it’s thriving. The platform has emerged as a trailblazer, proudly holding the title of the first licensed stablecoin on/off ramp in Africa.

So, what does that mean? Well, for starters, Yellow Card holds the Botswana Virtual Asset Service Provider license and a general financial services advice license in the CEMAC (Central African Economic and Monetary Community) region. These aren’t just fancy titles; they’re proof that Yellow Card is committed to playing by the rules while still pushing boundaries to make crypto accessible for everyone.

Compliance: The Backbone of Trust

If you’ve ever wondered why Yellow Card has gained the trust of millions across the continent, the answer lies in its rock-solid commitment to compliance. Let’s break it down:

- Global Standards: Yellow Card adheres to Anti-Money Laundering (AML) standards recognized globally. This ensures that the platform stays ahead of financial crime trends and fosters a secure environment for its users.

- FATF Travel Rule: You might think the “Travel Rule” has something to do with booking flights, but it’s actually a critical regulation for crypto transactions. Yellow Card ensures that all transactions comply with the Financial Action Task Force (FATF) guidelines, which aim to prevent illegal activities like money laundering and terrorism financing.

- Know Your Customer (KYC): Every Yellow Card user undergoes a thorough KYC process. This not only ensures compliance with local and international regulations but also builds trust within the ecosystem. Whether you’re trading stablecoins in Ghana or sending remittances in Rwanda, you can rest assured knowing the platform prioritizes safety.

Collaboration with Local Authorities

Yellow Card doesn’t just meet international standards—it goes the extra mile by working closely with local regulatory bodies. The company is registered with GoAML, a global anti-money laundering monitoring tool, and collaborates with Financial Intelligence Units (FIUs) in most of its operating jurisdictions.

Why does this matter? For starters, it means that Yellow Card can effectively report suspicious activities and assist in combating financial crimes. It also shows that the company isn’t just focused on profits; it’s committed to fostering a transparent and ethical crypto ecosystem in Africa.

A Blueprint for the Future

Africa’s regulatory environment is still evolving, and Yellow Card is helping to shape it. By working with governments, financial institutions, and international bodies, the company is setting a precedent for how crypto platforms can operate responsibly. This leadership is not just about ticking boxes; it’s about creating a foundation for sustainable growth in Africa’s crypto industry.

Investor Backing and Financial Strength

Yellow Card’s $50 million in funding has come from some of the most influential names in fintech, including Coinbase Ventures, CashApp, and Polychain Capital. This financial backing underscores the company’s credibility and potential.

These resources have allowed Yellow Card to expand its reach, innovate its products, and build trust in markets where financial services have historically been lacking.

How Yellow Card Redefines Cross-Border Payments

Yellow Card is revolutionizing the way Africans send and receive money across borders, addressing longstanding issues like high fees, currency volatility, and accessibility. Let’s take a closer look at how this platform is making a difference.

1. Tackling High Costs

Traditional remittance services have long been a thorn in the side of African consumers. Banks and money transfer operators often charge fees that can eat up to 8% of the amount sent—and that’s just the average. In some cases, like intra-African transfers, fees can climb as high as 20%. For a continent that receives an estimated $95 billion in remittances annually, these costs are staggering and unsustainable.

Yellow Card’s solution? Cutting out the middlemen. By leveraging stablecoins like USDT, USDC, and PYUSD, Yellow Card bypasses the traditional banking network, slashing fees to mere pennies on the dollar. For example, sending $200 with Yellow Card costs a fraction of the $16 average fee charged by traditional services, leaving more money in the hands of recipients.

This approach has been particularly transformative in countries like Ghana and Kenya, where high remittance fees have historically discouraged the use of formal channels. With Yellow Card, even low-income users can afford to send money home, whether it’s to pay for school fees, medical bills, or daily expenses.

2. Addressing Currency Volatility

Currency volatility is another major challenge faced by many African countries. Take Zimbabwe, for example, where hyperinflation has rendered the local currency nearly worthless. In such scenarios, stablecoins become a financial lifeline.

Yellow Card enables users to convert their local currency into stablecoins, protecting their wealth from rapid devaluation. Stablecoins are pegged to the U.S. dollar, offering a reliable store of value. A farmer in Zimbabwe, for instance, can sell their crops and immediately convert the proceeds into stablecoins, avoiding the risk of losing value overnight due to inflation.

This service is equally valuable in Nigeria, where the naira’s fluctuating value has created uncertainty for businesses and individuals alike. With Yellow Card, users can store their savings in stablecoins, hedge against currency risks, and plan for the future with greater confidence.

3. Integrating Local Payment Methods

Accessibility is a key factor in Yellow Card’s success. The platform’s integration with local payment methods—such as mobile money, bank transfers, and cash agents—ensures that even those in rural or underserved areas can benefit. Mobile money services like M-Pesa in Kenya and MTN Mobile Money in Uganda are deeply embedded in African communities, making them ideal partners for reaching the unbanked.

This seamless integration bridges the gap between the crypto ecosystem and everyday African consumers. For instance, a market vendor in rural Uganda can receive payments in stablecoins and cash out through mobile money without ever needing a bank account. This level of convenience has made Yellow Card an essential tool for users across the continent.

Economic Ripple Effects

Beyond individual stories, the broader economic impact of Yellow Card’s services is profound. Lowering remittance costs means more money stays in the hands of families, fueling local economies and reducing financial stress. According to a study by the World Bank, reducing remittance fees to 3% could unlock an additional $5 billion annually for African households.

Yellow Card is making this vision a reality. By putting more money in the hands of users, the platform is enabling better education opportunities, improved healthcare access, and greater financial independence for millions of Africans. It’s not just about making transactions cheaper and faster; it’s about empowering people to build better futures.

In a continent often left behind by traditional financial systems, Yellow Card is proving that innovation and inclusivity can go hand in hand. By tackling high costs, addressing currency volatility, and integrating local payment methods, the platform is not just redefining cross-border payments—it’s redefining possibilities.

Challenges and Future Opportunities for Yellow Card

Challenges

1. Fragmented Regulations Across African Countries

One of the biggest hurdles Yellow Card faces is the fragmented regulatory landscape across Africa. Each country has its own set of rules, and while some nations are relatively crypto-friendly, others still lack clear or cohesive regulations for digital currencies. For example, countries like Nigeria have seen massive crypto adoption, yet the regulatory environment remains volatile, with the Central Bank of Nigeria imposing restrictions on crypto transactions. On the other hand, nations like South Africa are more progressive in terms of crypto legislation but still face hurdles like inconsistent tax policies.

This fragmented regulatory environment makes it challenging for platforms like Yellow Card to operate smoothly across the entire continent, which is essential for a platform focused on cross-border payments. As regulations vary from one country to the next, Yellow Card must constantly adapt, which requires significant time, resources, and compliance strategies.

2. Limited Internet Access in Some Regions

Despite Africa’s rapidly growing internet penetration, there are still significant gaps in certain regions. According to data from the International Telecommunication Union (ITU), about 28% of Africa’s population does not have internet access. Rural areas in countries like Chad, Ethiopia, and Mozambique face even more significant challenges when it comes to reliable internet connectivity. This digital divide creates barriers for users in these regions who might be interested in using platforms like Yellow Card but simply don’t have access to the technology necessary to do so.

For instance, in many parts of sub-Saharan Africa, mobile internet is more accessible than broadband, but the quality of mobile data services can be inconsistent, leading to poor user experiences when trying to complete cryptocurrency transactions. Yellow Card, as a crypto exchange, depends heavily on internet connectivity for both transactions and education. As such, its expansion could be hindered by these connectivity issues.

3. Educating Users on the Benefits of Cryptocurrency

Despite the increasing interest in crypto, many people still don’t fully understand how it works or how it can benefit them. Crypto is often seen as too complex, and misconceptions abound. For example, a significant number of people in Africa still equate cryptocurrency with online scams or fraud due to past incidents involving Ponzi schemes or fraudulent investment offers.

Educating the unbanked and underbanked about how crypto works, how it can be used safely, and how it can improve their financial situations is an ongoing challenge. Yellow Card needs to focus on breaking down the barriers to understanding crypto. This can be done through educational campaigns, community workshops, and partnerships with local influencers who can demystify crypto for everyday users.

While some countries, such as Kenya and Nigeria, are home to vibrant crypto communities, others are still slow to adopt. According to a 2024 report by Chainalysis, Africa remains a global leader in peer-to-peer (P2P) crypto trading, but the understanding of its full potential still lags behind.

Opportunities

1. Scaling Operations to Reach Unbanked Populations

One of the biggest opportunities for Yellow Card lies in its ability to scale its operations and tap into Africa’s vast unbanked population. As of 2023, more than 60% of sub-Saharan Africa’s population remains unbanked, which means they don’t have access to traditional banking services. Yellow Card can fill this gap by offering low-cost financial services that do not require a bank account or credit score.

By offering easy-to-use mobile wallets, Yellow Card can onboard customers who would otherwise not have access to financial services. For example, the ease with which someone can transfer money across borders using crypto is a major draw, especially in regions where remittance fees are high, and banking infrastructure is limited. In Nigeria, for instance, Yellow Card allows users to send and receive crypto payments, bypassing expensive bank fees.

As mobile penetration continues to increase, platforms like Yellow Card can become more accessible, further driving financial inclusion. According to GSMA, mobile internet adoption in sub-Saharan Africa is expected to reach 50% by 2025, which means more people will be able to access Yellow Card’s services as long as the platform ensures its offerings are mobile-friendly.

2. Expanding into New Markets and Services

Yellow Card has the potential to expand its services beyond cross-border remittances. With crypto adoption rising steadily, Yellow Card could look into offering additional financial products, such as savings, loans, and insurance, which could be tailored to local needs and made more accessible through blockchain technology. These services could be built on stablecoins or other digital assets to ensure that they hold value in inflationary economies.

For example, countries like Zimbabwe, which have struggled with hyperinflation and a collapsing currency, could benefit from a platform like Yellow Card offering a stable store of value through cryptocurrencies like USDC. With Africa’s growing tech-savvy youth population, there’s also potential to introduce cryptocurrency-based savings programs, allowing users to earn yields on their holdings.

3. CBDCs Could Complement Yellow Card’s Offerings

Another exciting opportunity for Yellow Card comes with the rise of Central Bank Digital Currencies (CBDCs) across the continent. Countries like Nigeria and Ghana are already experimenting with CBDCs, and more are expected to follow suit. CBDCs offer the potential to seamlessly integrate with cryptocurrency services, creating an even more robust and efficient ecosystem for cross-border payments.

For example, if Nigeria’s digital Naira (eNaira) becomes more widely used, Yellow Card could incorporate it into its platform, allowing users to easily convert between the eNaira and other cryptocurrencies. This would provide more options for users and further enhance the convenience of the platform, positioning Yellow Card as a one-stop shop for digital currency and remittance services. The rise of CBDCs could create new regulatory frameworks that would help provide more clarity and stability to crypto operations across the continent, which would also work in Yellow Card’s favor.

4. Strengthening Partnerships and Collaborations

Yellow Card’s growth also hinges on forming new strategic partnerships with financial institutions, payment processors, and technology providers. By partnering with major players in the financial sector, it could expand its offerings, improve security, and make crypto more accessible to a broader audience. Collaboration with fintech companies already operating in the unbanked market could also help in increasing user adoption.

For instance, Yellow Card could partner with mobile money services like M-Pesa, which has over 30 million users across Africa, to allow people to buy crypto directly through mobile wallets. By expanding partnerships with mobile operators and local banks, Yellow Card could enhance its user base and reach customers in even the most remote areas.

Conclusion

Yellow Card is more than a crypto platform; it’s a movement for financial inclusion. By redefining cross-border payments, the company is giving millions of Africans access to tools that empower them financially. As Yellow Card continues to grow, it’s clear that the future of remittances in Africa is bright, digital, and inclusive.

For anyone tired of paying exorbitant fees or waiting days for a transaction to clear, Yellow Card’s message is clear: there’s a better way, and it’s already here.